In today’s digital age, cyber threats are a stark reality for businesses of all sizes. From data breaches to ransomware attacks, no organization is immune to these potentially devastating events. This article will delve into some major areas of cyber insurance, highlighting its crucial role in modern risk management strategies.

The Role of Cyber Insurance

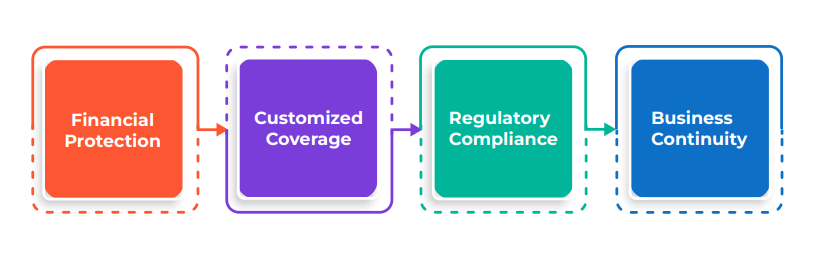

Cyber insurance plays a pivotal role in addressing and mitigating the consequences of cyber incidents, outlining four essential roles.

What does Cybersecurity Insurance Cover?

1st Party Damage

- Forensic Analysis: Costs to hire forensic experts to investigate and understand the breach.

- Legal Guidance: Expenses for legal consultants to navigate breach response laws and customer notifications.

- Credit Monitoring: Costs of providing credit monitoring to affected customers.

- Public Relations: Expenses to restore public trust in your organization.

- Cyber Extortion: Fees related to ransomware attacks under specific conditions.

- Business Interruption: Loss of revenue, customers, and system recovery costs due to a successful attack.

3rd Party Damage

- Re-issuing of Credit Cards: Costs borne by financial institutions.

- Stolen Intellectual Property: When your breach affects a third party.

- Stolen Licensed Property: Disclosure of licensed property after the breach.

- Stolen Documents: Including libelous/slanderous content about a third party.

What isn’t Covered by Cybersecurity Insurance?

- System Improvement: Costs for vulnerability fixes and system redesign

- Hardware Damage: Damage to physical hardware.

- Mental Distress: Executive, employee, or customer distress.

Application Process

The application process for cyber insurance involves submitting information on risk, data, security, and more.

- Policy Selection: Define the coverage you need.

- Industry and Revenue: Share your industry and annual revenues.

- Data Handling: Describe the type and volume of data you manage.

- Security Measures: Provide details on firewalls, system updates, encryption, and more.

- Device and Employee Policies: Explain your policies on third party and employee devices.

What are Insureds’ Responsibilities?

After obtaining cybersecurity insurance, individuals and businesses aim to avoid using it by maintaining strong security measures. Insurance providers typically require minimum-security controls such as MFA, EDR, encryption, backups, awareness training, patch management, email filtering, access controls, network segmentation, BCP/DR/IR plans, and more. Some insurers even offer cyber assurance security tools to reduce the risk of an attack.

Real-World Scenarios

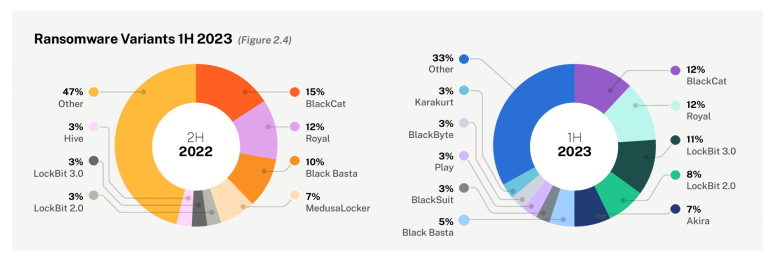

A cyber insurance firm reported a sharp rise in claims during H1 2023, attributing it to increased damages from cyberattacks. Ransomware, accounting for 12% more claims than the previous year, was a major driver of this surge. May recorded the highest number of ransomware claims ever in Coalition’s history. Large firms with revenues over $100 million experienced a 20% uptick in cyber incidents. Funds transfer fraud claims increased by 15%. However, business email compromise claims decreased by 15%, providing a rare positive note. Cyber insurance is a rapidly expanding industry, predicted to reach $50 billion by 2030.

Source: https://shorturl.at/rxRYZ

IBM’s latest Cost of a Data Breach report discovered that, in 2023, the average cost of a data breach globally reached an all-time high of $4.45 million. This figure represents a 2.3% increase from the previous year and a 15.3% rise from 2020.

A Wall Street analyst said the losses MGM Resorts International is experiencing from a cyberattack on the company’s hotel-casino operations in eight states could be covered by a $200 million cyber insurance policy covering ransom payments and business interruption.

University of California, San Francisco, faced a ransomware attack that encrypted critical data, including COVID-19 research. Cyber insurance helped cover expenses, facilitating data recovery, legal matters, and ensuring uninterrupted healthcare and research operations during the pandemic.

Final Thoughts

In tandem with technological progress, cybercriminal tactics evolve, emphasizing the need for proactive measures by individuals and organizations. Cyber insurance provides financial security, mitigating the impact of unforeseen cyber incidents. Investing in cyber insurance safeguards digital assets and ensures confidence in navigating the digital era’s challenges.

Author

Praveenkumar Jothi

Praveen is a cybersecurity lead with 11 years of experience in the IT industry. His expertise encompasses IT infrastructure, Identity and Access Management (IAM), and the last five years have been dedicated to Governance, Risk, and Compliance (GRC). Additionally, Praveen is an active traveler and motorcycle enthusiast. He channels his passion for biking by running a biking club in the state.